The Scapia Federal Bank credit card is a lifetime-free travel card with two features that genuinely matter: zero forex markup on international spends, and unlimited domestic lounge access once you spend Rs. 20,000 in a billing cycle. I have carried it as my main card for a little over three months, moving nearly all my day-to-day payments onto it. In that time I have built up around 16,000 Scapia Coins, worth roughly Rs. 3,200.

That last bit is the honest catch. Coins are worth Rs. 0.20 each, and you can only spend them inside the Scapia app, on flights, hotels, buses, trains, or visa fees. No cashback, no statement credit, no Amazon vouchers. If you travel, that is fine. If you do not, the rewards are dead weight.

So this review is less about whether the card is good in the abstract and more about who it is actually for. I think the answer is narrower than the marketing suggests, but for the right person, and I am probably one of them, it is hard to beat at Rs. 0 a year.

Why I am writing this

Most Scapia reviews online are written by credit card reviewers who applied for the card just to review it. This one is not. I got the Scapia card because I wanted a proper travel and forex card. I currently use an HDFC forex card and I do not think it is efficient enough, so Scapia is the card I am planning to actually travel with next.

I have the dual setup: the Visa variant and the RuPay variant, both lifetime free, sharing one credit limit. Most of my routine spending goes through the credit card. I have not used the airport lounge yet, so I will be upfront about that section and tell you what is documented rather than pretend I have tested it. Everything below about fees, reward rates, and thresholds is sourced and linked.

What the Scapia card actually is

Scapia is a co-branded credit card. The travel fintech Scapia runs the app and the experience; Federal Bank issues the card and does the underwriting. You apply entirely through the Scapia app, and there is no joining fee and no annual fee, ever.

The pitch is simple. Instead of a points programme you have to decode, Scapia gives you three things: zero forex markup, unlimited domestic lounge access on a spend condition, and rewards as Scapia Coins you redeem for travel inside their app.

Quick note if you have been searching around: Scapia card, Scapia credit card, federal bank Scapia credit card, and Scapia forex card all mean the same product. There is no separate Scapia travel card or Scapia forex card sold on its own.

Onboarding: genuinely the easy part

This is where the card earns its reputation. Onboarding is fully online through the app. You download it, go through the steps, complete video KYC, and the virtual card is ready almost immediately, so you can start using it before the plastic arrives.

My own experience matched what most people report. The app onboards you quickly and absolutely online, the virtual card is live fast, and the physical card lands at your address in about seven days. Federal Bank quotes 2 to 5 working days for the physical card; a week including dispatch felt right to me.

One real warning, though it did not happen to me. A lot of applicants get to the final address step and are told their PIN code is not serviced by Federal Bank, even when there is a Federal Bank branch nearby. The app lets you go through the whole application and only flags this at the very end. If you are outside a major city, treat approval as uncertain until it actually clears.

Rewards: Scapia Coins, explained without the spin

This is the part the app makes more confusing than it needs to be.

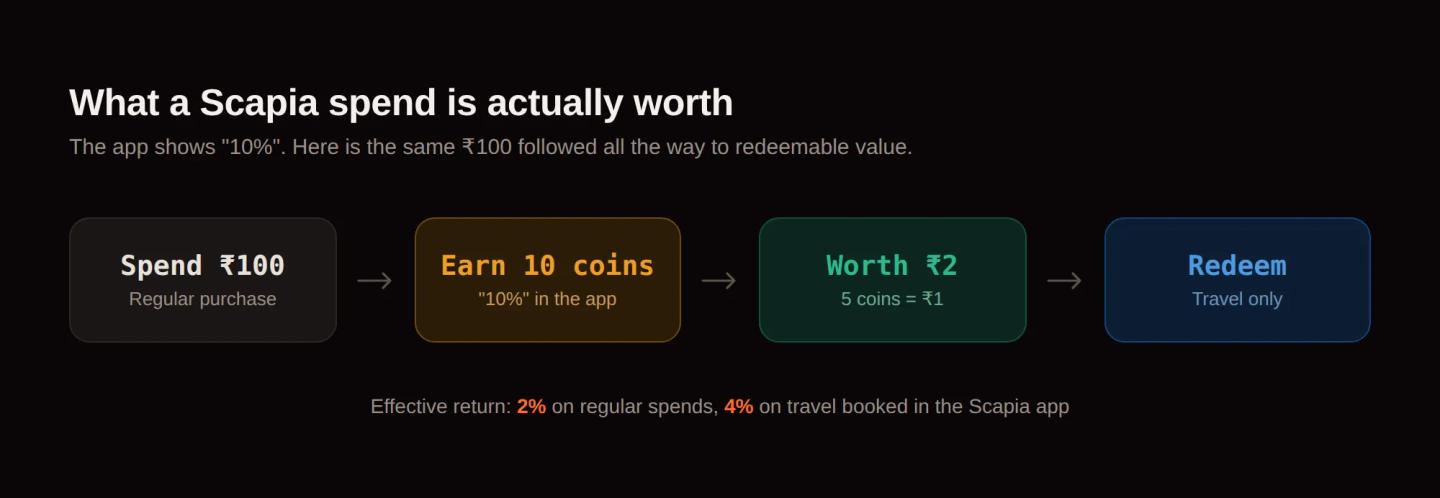

Scapia advertises 10% rewards on regular spends and 20% on travel. Those numbers are coins, not rupees. The conversion is fixed: 5 Scapia Coins = Rs. 1, or Rs. 0.20 per coin. Do the maths and the real picture looks like this.

| Spend type | Scapia Coins | Real value |

|---|---|---|

| Regular online and offline spends | 10 coins per Rs. 100 | 2% |

| Travel booked inside the Scapia app | 20 coins per Rs. 100 | 4% |

| International spends | 0 coins | 0% |

A worked example makes it concrete. For every Rs. 1,000 you spend on a regular purchase, you earn 100 coins, which redeem for Rs. 20. The same Rs. 1,000 booked as travel inside the Scapia app earns 200 coins, worth Rs. 40. Spent abroad, it earns nothing.

A 2% base rate on a lifetime-free card is good. The 4% on travel only applies when you book through the Scapia app itself, which is the trade-off: better rewards, but inside their walls.

What does not earn coins is worth knowing before you apply. As of the February 2026 update, utilities and insurance no longer earn any rewards, and they do not count toward your lounge spend either. Rent, fuel, education, government payments, gift cards, and wallet top-ups are also excluded. On the RuPay variant, transactions under Rs. 500 do not earn coins. So the 2% applies to ordinary shopping, dining, and similar spends, not to the bills a lot of people hope to route through a card.

I have about 16,000 coins after three months of regular use, which is roughly Rs. 3,200 in redeemable value. That tracks with a 2% rate on day-to-day spending.

Interactive Scapia reward calculator. Enter a spend amount in rupees to see the Scapia coins earned and their rupee value back, for regular spends, travel booked in the Scapia app, and international spends.

Regular spends · 2%

1,000 coins → ₹200

Travel via app · 4%

2,000 coins → ₹400

International · 0%

0 coins → ₹0

Regular spends earn 10 coins per ₹100, travel booked in the Scapia app earns 20 per ₹100, international spends earn nothing. 5 coins = ₹1. Open in full →

Scapia Points Redemption

The complaint you will see most often online is that Scapia Coins lock you into the ecosystem. That is true, and I will not pretend otherwise. But the redemption mechanics themselves are unusually good, and they are easy to miss.

Coins are redeemed only inside the Scapia app, against flights, hotels, buses, trains, and visa fees. No cashback, no statement credit.

Here is the good part: Scapia lets you redeem 100% of a booking with coins. Most bank reward programmes cap point usage at around 50% of a ticket price and make you pay the rest in cash. Scapia does not. There is also no cap on how many coins you can earn or redeem.

To put it in real terms: if I book a Bengaluru-Kolkata flight worth Rs. 6,000 to 7,000 tomorrow, I can pay most or all of it straight from my coins, and the rest in cash. I do not need to transfer points to an airline programme, download a separate miles app, or get bounced to some third-party redemption portal. The points live in the same app I would book the flight in anyway. After never having had a travel card give me benefits like this, that is the part I find genuinely refreshing.

That convenience is the honest counterweight to the lock-in. Yes, the coins only work for travel. But if you travel, redeeming them is frictionless in a way most miles cards just are not. If you do not travel, none of this rescues the card for you.

Zero forex markup: the actual headline feature

Most Indian credit cards charge a forex markup of around 2 to 3.5% on international transactions, plus GST on that markup. On a Rs. 1,00,000 spend abroad, that is a few thousand rupees gone before you have earned a single reward point.

Scapia charges 0% forex markup. That is normally a premium-card feature, and getting it on a lifetime-free card is the real reason I got this card.

Two honest caveats. First, international spends earn no coins, so you save on the markup but earn nothing back. Second, zero markup is the bank fee, not the exchange rate. Scapia uses a network rate that is competitive but not something you should assume is the exact mid-market rate. If you want to see how far a card rate sits from the real mid-market rate, that is exactly the kind of comparison CurrencyCalculator's currency converter is built to make visible.

For context, even a super-premium card like HDFC Diners Black still carries roughly a 2% forex markup. Reward points on those cards partly offset it, but the net cost is rarely zero. Scapia net forex cost genuinely is zero. This is the feature I most want to put to the test on my next trip, because forex markup is where my current HDFC forex card has been quietly costing me.

Lounge access and airport privileges

Unlimited domestic airport lounge access is a real benefit here, but it comes with a spend condition that changed recently, and a lot of older reviews still quote the old number.

To unlock lounge access, you have to spend Rs. 20,000 in the preceding billing cycle. This can be across both the Visa and RuPay variants combined. The threshold was Rs. 10,000 until 27 February 2026, when Scapia doubled it. Excluded categories like rent, utilities, fuel, and insurance do not count toward it. Access typically activates 3 to 5 working days after your statement date once you have met the spend.

Lounge access is one of four Airport Privileges you pick from each time you fly: lounge, or shopping, dining, or spa at the airport. If you choose the shop or dine option, you spend at a listed airport outlet and get up to Rs. 1,000 back as coins at metro airports, or Rs. 500 at smaller ones. There is also a newer international airport benefit worth up to Rs. 2,000 in coins, but it unlocks only on a Rs. 50,000-plus international flight booking made through the Scapia app, which is a steep gate.

One genuine friction point, which I have seen raised over and over by other users: the airport shopping benefit is not automatic. You have to open the app, pick the privilege, and activate the specific outlet before you pay. Miss that step and you do not get reimbursed, even if you try to claim afterwards. It works, but it asks something of you each time.

I have not used the lounge yet. I know it needs the monthly spend hit, and that is the honest status. I will update this section once I have.

Apply for the Scapia Credit Card here.

Eligibility: the things that get applications rejected

Scapia approvals are handled by Federal Bank, and the rejections tend to come from a few specific places rather than from income alone.

- A healthy credit score helps. A CIBIL score around 750-plus is the comfortable zone. People report rejections even above 760, often tied to too many recent credit enquiries.

- PIN code servicing. Federal Bank does not serve every location, and the app will not tell you until the final step.

- Recent credit enquiries. Several rejections cite credit enquiries in the last six months as the reason.

- Existing Federal Bank cards. This used to be a hard block. Reports through 2025 suggest Federal Bank now allows holding multiple cards, though some applicants with a top-tier Federal card still get rejected or get a low limit. It is inconsistent, so do not count on it.

If you are rejected at the PIN-code step, it is worth trying again in a few months as Federal Bank expands coverage.

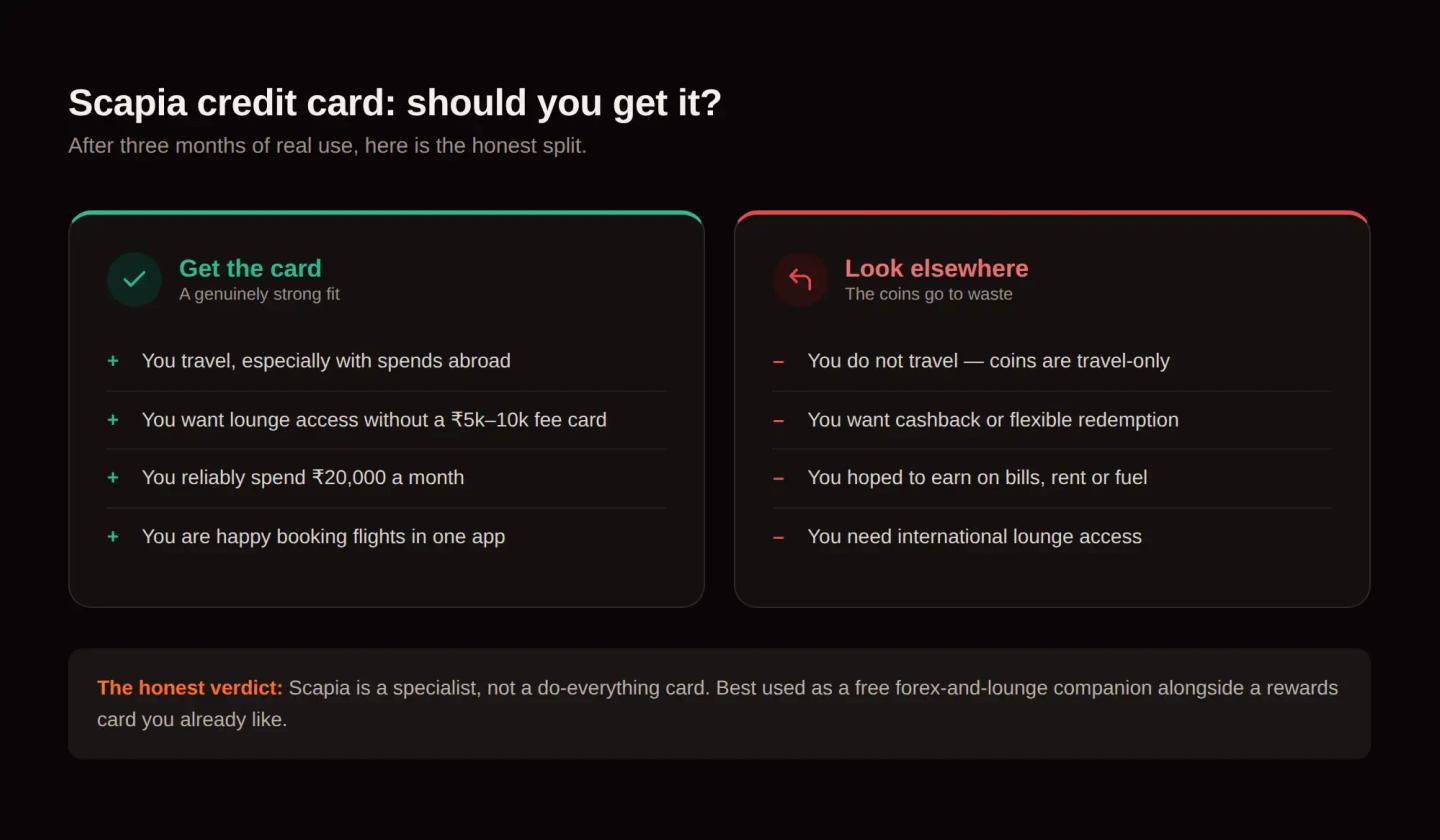

So, who is this card actually for?

After three months of real use, here is my honest read.

Get the Scapia card if:

- You travel, even occasionally, and especially if you spend abroad. Zero forex markup alone justifies keeping it in your wallet.

- You want unlimited domestic lounge access without paying Rs. 5,000 to 10,000 a year for a premium card, and you reliably spend Rs. 20,000 a month.

- You are comfortable booking flights and hotels inside one app, since that is where your coins go.

- You want a clean, lifetime-free card with one of the smoothest onboarding experiences in India.

Look elsewhere if:

- You do not travel. The coins are travel-only and become dead value.

- You want cashback or flexible redemption. Scapia has neither.

- You were hoping to earn rewards on utilities, insurance, rent, or fuel. Those are excluded.

- You need international lounge access. The card does not offer it.

- Your main spend is abroad and you already have a premium card you love. Comparing Scapia to an HDFC Infinia or Diners Black is not quite fair, since they are different classes of card.

That last point is the one I would underline. Scapia is not trying to be your only card. It is a specialist. As a free, zero-forex, lounge-access companion card, it is excellent. As a do-everything rewards card, it is not, and it does not pretend to be.

My verdict after three months: it is a decent card, and the real test for me comes on my next big trip. I got it specifically as a forex and travel card to replace one I have outgrown, and whether large travel spends actually turn into rewards I value is something only a real trip will tell me. I will update this review once I have travelled with it. I think six months in, with a trip behind me, I will truly know if it is worth it.

Is the Scapia credit card good?

For travellers, yes. Zero forex markup, unlimited domestic lounge access, and a 2% base reward rate on a lifetime-free card is a strong combination. For non-travellers it is weak, because Scapia Coins can only be redeemed for travel.

Is the Scapia credit card lifetime free?

Yes. There is no joining fee and no annual fee, and no minimum spend to keep the card free. The Rs. 20,000 monthly spend only affects lounge access, not the card free status.

What is the Scapia Coins conversion rate?

5 Scapia Coins equal Rs. 1, so each coin is worth Rs. 0.20. You earn 10 coins per Rs. 100 on regular spends, an effective 2%, and 20 coins per Rs. 100 on travel booked in the Scapia app, an effective 4%.

Can I redeem Scapia Coins for cashback?

No. Coins can only be used inside the Scapia app for travel bookings such as flights, hotels, buses, trains, and visa fees. There is no cashback or statement credit option.

What is the spend requirement for Scapia lounge access?

You have to spend Rs. 20,000 in the preceding billing cycle, combined across the Visa and RuPay variants. This threshold rose from Rs. 10,000 on 27 February 2026. Excluded categories like rent, utilities, and fuel do not count.

Why do Scapia card applications get rejected?

Common reasons include a PIN code Federal Bank does not service, a credit score below the bank cut-off, too many recent credit enquiries, or in some cases an existing Federal Bank card. The app often only flags a servicing issue at the final address step.